Canada remains a preferred destination for Indian students pursuing higher education, with over 230,000 Indian students enrolled in Canadian institutions as of 2026. The cost of education-ranging from CAD 20,000 to CAD 60,000 annually depending on the program-presents a significant financial commitment. For families without tangible assets to pledge, securing an abroad education loan becomes a practical necessity rather than a choice.

Non-collateral loans have evolved from niche products to mainstream financing options. This guide examines the current landscape, eligibility requirements, and strategic considerations for securing these loans in 2026.

Understanding Non-Collateral Education Loans

A non-collateral foreign education loan from India does not require borrowers to mortgage property, fixed deposits, or other tangible assets. Instead, lenders evaluate creditworthiness through alternative parameters: academic profile, university ranking, program reputation, co-applicant income stability, and future earning potential.

The shift toward these products reflects two market realities. First, many creditworthy families lack liquid assets to pledge. Second, lenders have refined risk assessment models that can predict repayment probability without relying exclusively on collateral. This has opened access to students who previously would have been excluded from formal financing channels.

However, this convenience carries trade-offs. Interest rates on non-collateral loans typically run 200-300 basis points higher than secured loans. Loan quantum is capped-usually between INR 40 lakhs and INR 75 lakhs depending on the lender and program tier.

The 2026 Lending Environment

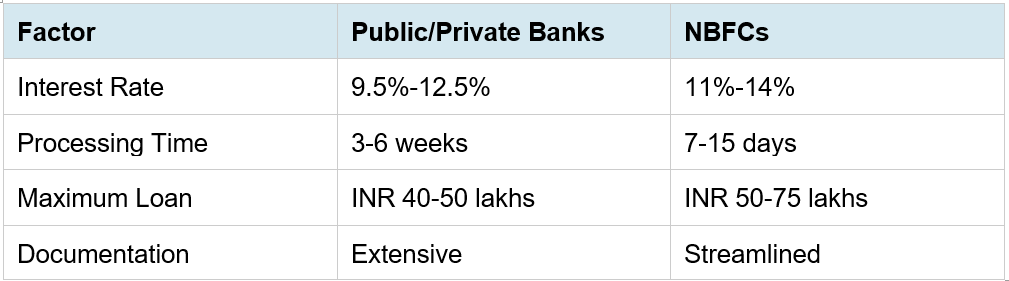

The overseas education loan market has experienced notable shifts in early 2026. Public sector banks, historically conservative with non-collateral lending, have marginally expanded exposure to this segment following regulatory guidance on education finance. However, their processes remain documentation-intensive and approval timelines extend to 4-6 weeks.

Non-Banking Financial Companies (NBFCs) continue to dominate the non-collateral space, offering faster processing—typically 7-10 business days—and more flexible eligibility criteria. Their digital-first approach streamlines application workflows, though this speed comes with marginally higher interest rates. International lenders have entered the Indian market through partnerships with local facilitators, targeting students admitted to Tier-1 Canadian universities. These products

often feature in-study moratoriums and graduated repayment structures, though they require strong co-applicant profiles.

Eligibility Framework

Lenders assess non-collateral loan applications through a multi-factor framework. Academic credentials form the foundation: admission to recognized Canadian universities (preferably those in the QS Top 500) carries significant weight. Programs in STEM fields, business, and healthcare receive more favorable consideration due to employment outcomes data.

Co-applicant profile directly impacts approval probability. Most lenders require a parent or guardian as co-applicant, evaluating their income stability, employment history, and existing debt obligations. A minimum annual income of INR 4-6 lakhs is standard, though this varies by lender and loan amount. Credit history of the co-applicant undergoes thorough scrutiny-defaults or irregular repayment patterns on existing loans materially affect eligibility.

Age restrictions apply: students typically must be between 18-35 years at the time of application. Some lenders impose upper age limits on co-applicants, generally capping at 65 years.

Lender Categories: Strategic Differences

The choice between public sector banks, private banks, and NBFCs involves evaluating more than just interest rates. Each category operates under distinct paradigms that affect the borrowing experience.

Public sector banks offer lower interest rates but operate with rigid eligibility criteria and slower turnarounds. Private banks occupy a middle ground, with moderate rates and faster processing than their public counterparts. NBFCs provide the fastest approvals and highest loan amounts but at premium interest rates. The optimal choice depends on your timeline, loan requirement, and risk profile.

Loan Coverage Scope

Non-collateral loans for Canada typically cover tuition fees, accommodation costs, travel expenses, and living expenses for the duration of the program. Some lenders include pre-departure expenses such as visa fees, examination fees (IELTS, TOEFL), and university application costs within the loan amount.

Living expense coverage varies by lender. Conservative estimates place monthly living costs in major Canadian cities at CAD 1,200-1,800. Lenders generally sanction 80-100% of the total cost of attendance as declared by the university, subject to their internal caps. It is prudent to factor in a 10-15% buffer for contingencies and exchange rate fluctuations.

Application Process

The application workflow begins with university admission confirmation. Lenders will not process loan applications without a formal admission letter specifying the program, duration, and fee structure. Once this is secured, gather financial documents: last three years’ income tax returns for the co-applicant, bank statements for the past six months, salary slips, and proof of existing assets or liabilities.

Academic credentials include all mark sheets from Class 10 onward, standardized test scores (GRE, GMAT, IELTS as applicable), and any relevant work experience certificates. The admission letter should clearly indicate the total program cost in CAD and its INR equivalent at current exchange rates.

Professional education loan consultants can reduce processing friction by ensuring documentation completeness before submission. This step often proves decisive in approval timelines, as incomplete applications trigger repeated back-and-forth that extends the process by weeks.

Critical Considerations

Three factors warrant careful attention during the decision process. First, understand the moratorium structure. Most non-collateral loans offer a grace period of six months to one year post-course completion before EMI payments commence. This window is critical for securing employment and stabilizing finances after graduation. Clarify whether interest accumulates during the moratorium and if partial payments are permitted.

Second, assess prepayment policies. Some lenders impose prepayment penalties on non-collateral loans, while others allow partial or full prepayment without charges after a minimum lock-in period. If you anticipate early repayment capability-through parental support or early employment-this clause becomes material.

Third, evaluate tax benefits. Interest paid on education loans qualifies for deduction under Section 80E of the Income Tax Act, with no upper limit on the amount claimed. This benefit extends for up to eight years or until interest is fully repaid, whichever is earlier. Maintain proper documentation of interest payments for tax filing purposes.

Strategic Approach to Financing

Non-collateral education loans have democratized access to international education, but they require informed decision-making. The variance in interest rates, processing timelines, and loan terms across lenders makes comparative analysis essential rather than optional. Students in Hyderabad and across India should begin the loan exploration process at least three to four months before their intended program start date to account for documentation, processing, and potential delays.

Working with experienced advisors can streamline this process significantly. Loan Blaze Financial Consultant provides end-to-end support for students navigating foreign education loan from India requirements, from lender comparison to documentation assistance and application tracking. Their advisory model focuses on matching borrower profiles with appropriate lender products rather than pushing predetermined solutions.

Need guidance on securing a non-collateral education loan for Canada?

Connect with Loan Blaze to evaluate your eligibility across multiple lenders, understand documentation requirements specific to your profile, and structure a financing plan aligned with your academic timeline. Visit loanblaze.in or schedule a consultation to discuss your education financing needs.

Leave a Reply